American Families Plan Tax Compliance Agenda By STEVE TOSCHER and SANDRA BROWN

On May 20, 2021, the U.S. Treasury published a report entitled “The American Families Plan Tax Compliance Agenda.”[1] The 22-page report reiterates previously-announced proposals by the Biden administration focused on increasing and improving tax compliance, including increasing information reporting by banks with respect to cryptocurrencies and additional financial transactions, and increasing the budget of the IRS for modernization, security and to help detect tax evasion and to narrow the tax gap.

Tax Gap

The tax gap is the difference between the amount of tax owed by taxpayers for a given year and the amount that is actually timely paid for that same year.[2] As of 2019, the tax gap reached nearly $600 billion and is anticipated to rise to close to $7 trillion over the course of the next decade if left unaddressed – leaving roughly 15% of taxes owed going uncollected.[3]

The tax gap has three distinct elements:

- Taxpayers who fail to file returns in a timely manner (the “nonfiling” tax gap);

- Those who underreport income or overclaim deductions (the “underreporting” tax gap); and

- Those who underpay taxes despite reporting obligations in a timely manner (the “underpayment” tax gap)

Those who fall within the “underreporting” category account for almost 80% of the overall tax gap problem.[4]

American Families Plan Initiatives

The American Families Plan proposes initiatives that are estimated to raise $700 billion in additional tax revenue over the next decade and $1.6 trillion in the second decade trillion.[5]

There are four categories in the agenda focused on efforts to increase tax compliance.

- Increase the resources of the IRS to pursue noncompliant taxpayers and better serve those who are fully compliant;

- Increase the information reporting, including leveraging information that financial institutions already collect to shed light on those taxpayers who misreport income derived from opaque categories;

- Overhauling antiquated technology to help leverage data analytic tools; and

- Regulate paid tax preparers and increasing penalties for those who intentionally commit malfeasance.

Increasing IRS Resources

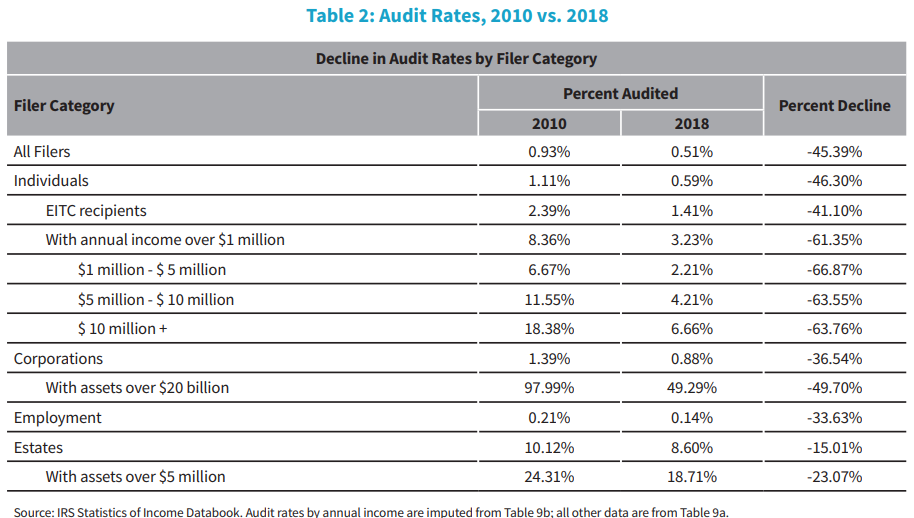

It is no secret that the IRS’s overall budget declined by 18.5% between FY 2010 and FY 2021,[6] and its enforcement budget decreased by 15% over this time period, leading to a 20% decline in the IRS workforce.[7] These losses have been most significant for revenue officers who collect taxes (50% decrease) and revenue agents who audit complex returns (35% decrease).

The share of audited returns declined by nearly 45% between 2010 through 2018. There has also been a steep decline in audit rates across all filing categories. The share of corporate income tax, individual income tax, estate tax, and employment tax returns examined by auditors have all dropped in the last decade.

The Biden administration proposes providing the IRS with nearly $80 billion in additional resources over the next decade. As noted in the report, the additional funding is intended, along with other things, to enable the IRS to hire new “specialized enforcement staff” and “revitalize the IRS’s examination of large corporations, partnerships, and global high-wealth and high-income individuals.” Specifically, the proposed budget increase will enable the IRS to focus its enforcement scrutiny on high-income taxpayers and their businesses – arguably, significant contributors to the overall tax gap.

Increasing Information Reporting: Form 1099-INT and Cryptocurrency

Increased third-party information reporting is one of the more efficient and resource savings way to increase the overall tax reporting compliance rate as existing empirical evidence has confirmed.[8]

One proposal is for financial institutions to report additional data to the IRS regarding its customers’ financial accounts on already existing information returns, such as the Form 1099-INT, that would provide the IRS with specifics as to gross inflows and outflows on all business and personal accounts from financial institutions, including bank, loan, and investment accounts but carve out exceptions for accounts below a low de minimis gross flow threshold.[9]

Another proposal is to expand tax compliance to cover cryptocurrency reporting requirements for investors, cryptocurrency exchanges, and payment service accounts that accept cryptocurrencies. Businesses that receive cryptocurrency with a fair market value of more than $10,000 would be required to report these transactions.

Overhauling Outdated Technology

The IRS still relies on Individual and Business File Systems that date back to the 1960s.[10] Modernizing the IT would not only be more efficient, secure and cost effective, but is also intended to enable the IRS to better identify suspect tax filings.[11] For example, by comparing returns to similarly situated taxpayers and historical filings in a way that the current IRS IT system does not allow. These resources would also support efforts to meet threats to the security of the tax system like the 1.4 billion cyberattacks the IRS experiences annually.

Regulating Paid Tax Preparers

With the IRS’s focus on “enablers” which can often reach large swaths of taxpayers in one investigation rather than a single taxpayer at a time, the report also identifies proposals intended to provide the IRS with the authority to regulate and establish minimum competency standards for all paid tax preparers.[12]

Increased Tax Enforcement

While we may not see all of the above proposals enacted into law, the message of the American Families Plan agenda is clear. The IRS is focused on increased enforcement of high-net-worth individuals. Increased audits, heightened scrutiny, and a closer look at non-compliance by those who are viewed as contributors to the tax gap is the clear message.

Steven Toscher is a Principal at Hochman Salkin Toscher Perez P.C., and specializes in civil and criminal tax litigation. Mr. Toscher is a Certified Tax Specialist in Taxation, the State Bar of California Board of Legal Specialization and represents clients throughout the United States and elsewhere involving federal and state, civil and criminal tax controversies and tax litigation.

Sandra R. Brown is a Principal at Hochman Salkin Toscher Perez P.C., and former Acting United States Attorney, First Assistant United States Attorney, and the Chief of the Tax Division of the Office of the U.S. Attorney (C.D. Cal). Ms. Brown specializes in representing individuals and organizations who are involved in criminal tax investigations, including related grand jury matters, court litigation and appeals, as well as representing and advising taxpayers involved in complex and sophisticated civil tax controversies, including representing and advising taxpayers in sensitive-issue audits and administrative appeals, as well as civil litigation in federal, state and tax court.

[1] https://home.treasury.gov/news/press-releases/jy0188

[2] U.S. Department of Treasury, “The American Families Plan Tax Compliance Agenda,” May 20, 2021, at 1.

[3] Id. at 3.

[4] Id. at 4.

[5] Id. at 2.

[6] IRS Statistics of Income, “Table 31: Collection Costs, Personnel, and US Population,” IRS Databook, 2019.

[7] Supra note 1 at 11.

[8] GAO, “Multiple Strategies are Needed to Reduce Noncompliance: Statement of James R. McTigue, Jr. Director, Strategic Issues,” 2019. Dina Pomeranz, “No Taxation Without Information: Deterrence and Self-Enforcement in the Value Added Tax,” American Economic Review, 105(8), 2015.

[9] Supra note 1 at 19.

[10] GAO, “IRS Needs to Take Additional Actions to Address Significant Risks to Tax Processing,” GAO-18-298, 2019.

[11] Id. at 2.

[12] Id. at 21.