TAXLITIGATOR Blog

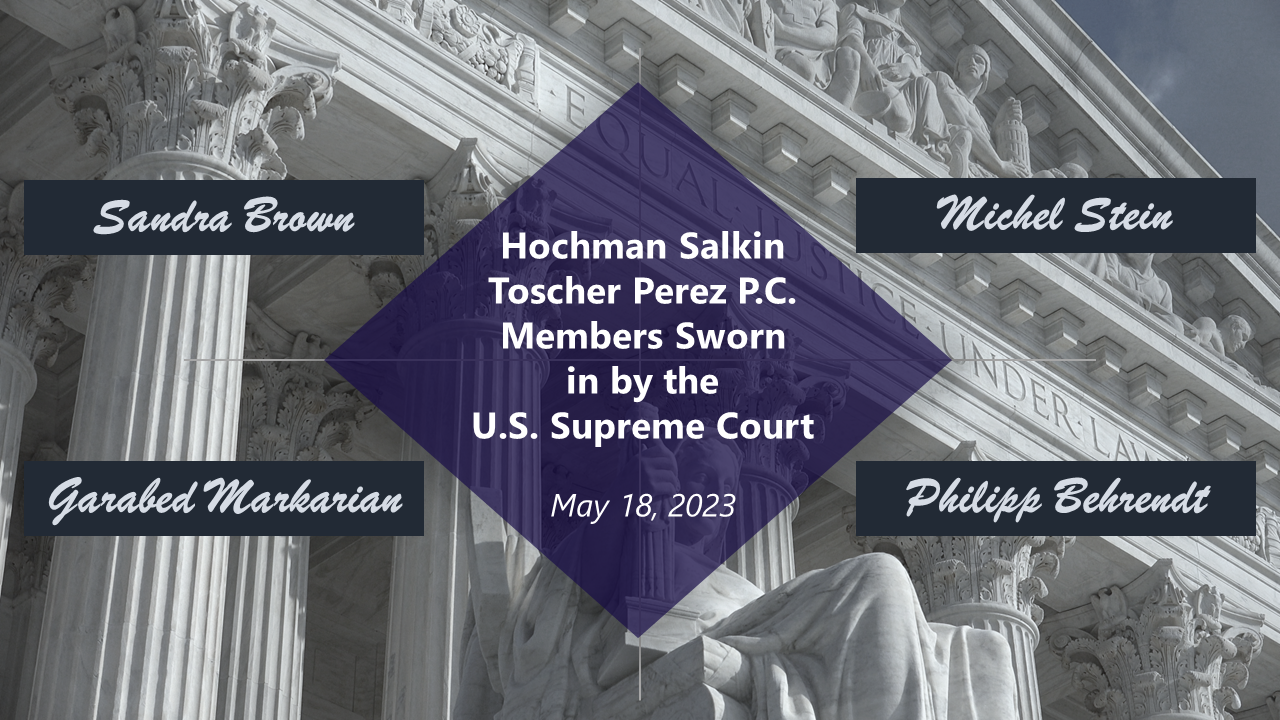

California Lawyers Association – Members of Hochman Salkin Toscher Perez P.C. Sworn in by the U.S. Supreme Court

We are very pleased to announce that on May 18, 2023, following the success of the firm’s participation in the Taxation Section of the California Lawyers Association’s “DC Delegation,” the following principals and associates of Hochman Salkin Toscher Perez P.C. were sworn in as members of the Supreme Court of the United States by Chief […] Read More…

Read MoreDENNIS PEREZ, ROBERT HORWITZ, and JONATHAN KALINSKI to Speak at Upcoming CPA Academy Webinar

We are pleased to announce that Dennis Perez, Robert Horwitz and Jonathan Kalinski will be speaking at the upcoming CPA Academy webinar “Resolving Employment Tax Disputes,” Tuesday, June 6, 2023, 2:00 p.m. – 3:00 p.m. (PST). The IRS is increasing civil and criminal enforcement against taxpayers who fail to comply with withholding and remitting of employment […] Read More…

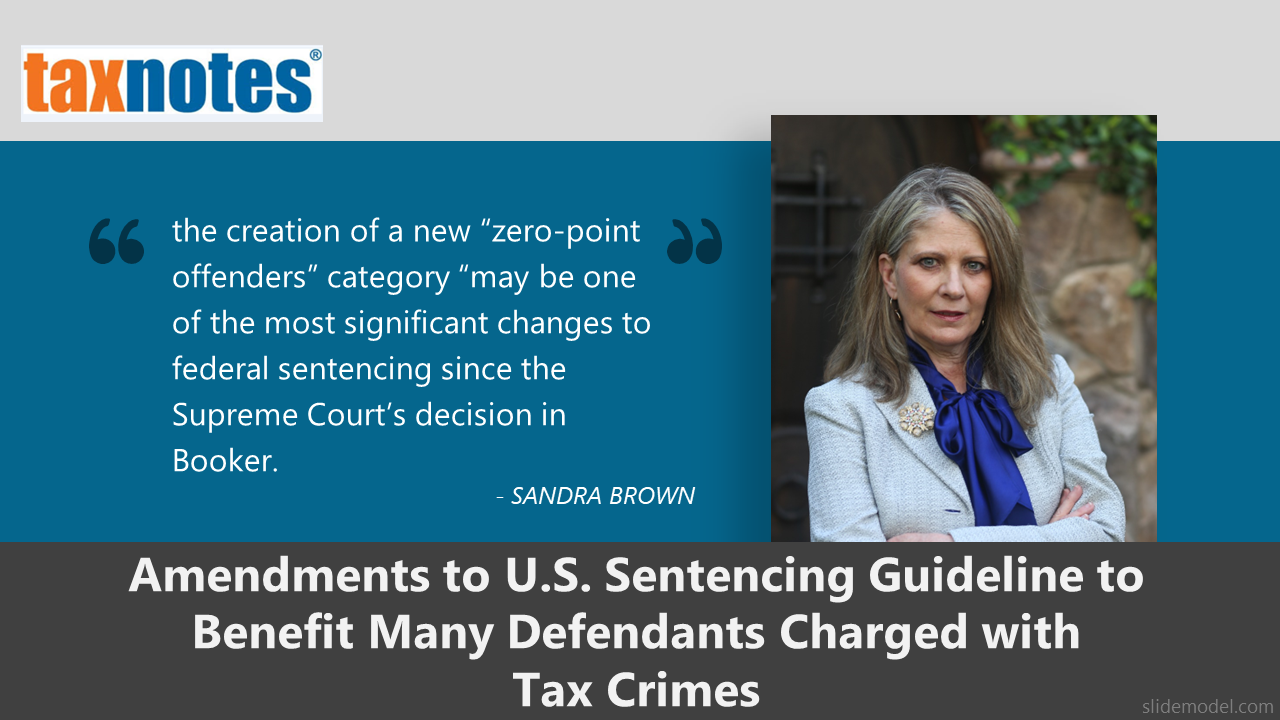

Read MoreSANDRA BROWN Quoted in Tax Notes

An amendment to the U.S. Sentencing Guidelines Manual that takes effect November 1 will include a new two-level reduction for true first offenders having their first contact with the criminal justice system. The amendment, subject to certain exceptions, will apply to offenders with no criminal history points, including offenders with no prior convictions. In adopting this […] Read More…

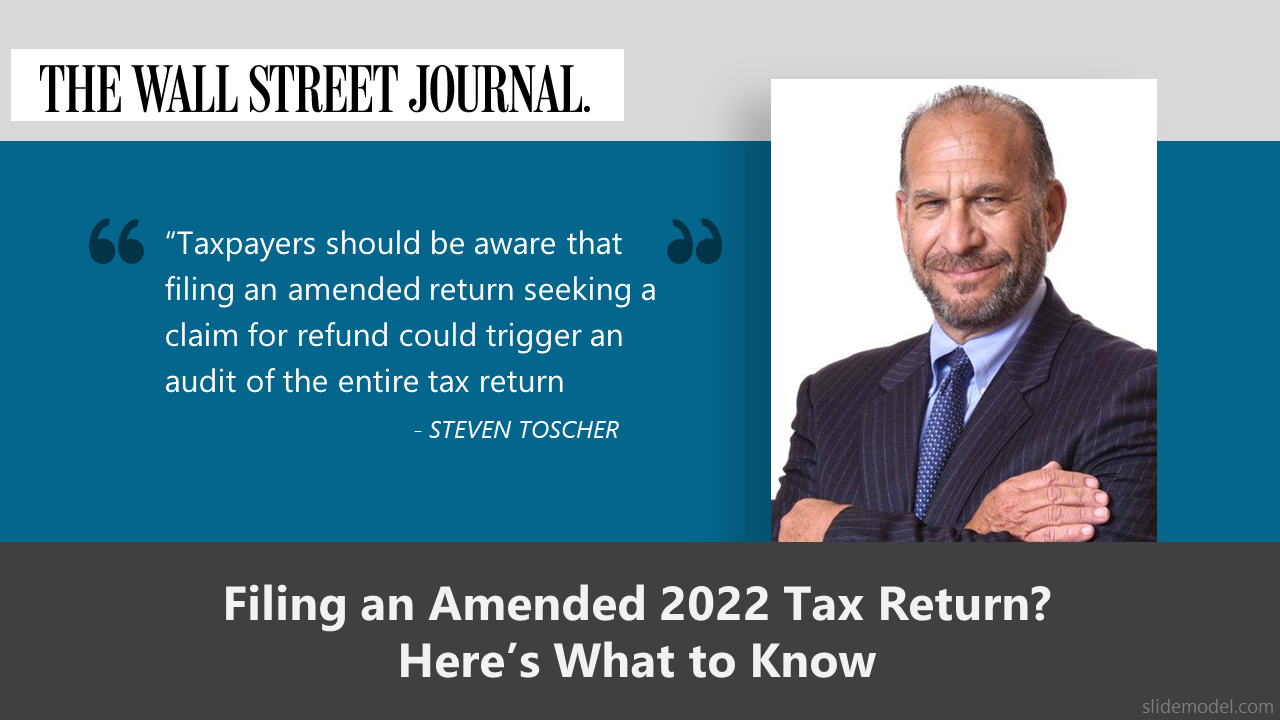

Read MoreSTEVEN TOSCHER Quoted in Wall Street Journal

I thought you would be interested in the following story from The Wall Street Journal. Click Here for Link to the Article Download the Wall Street Journal app here: WSJ. Steven Toscher specializes in civil and criminal tax controversy and litigation. He is a Certified Tax Specialist in Taxation, the State Bar of California Board of […] Read More…

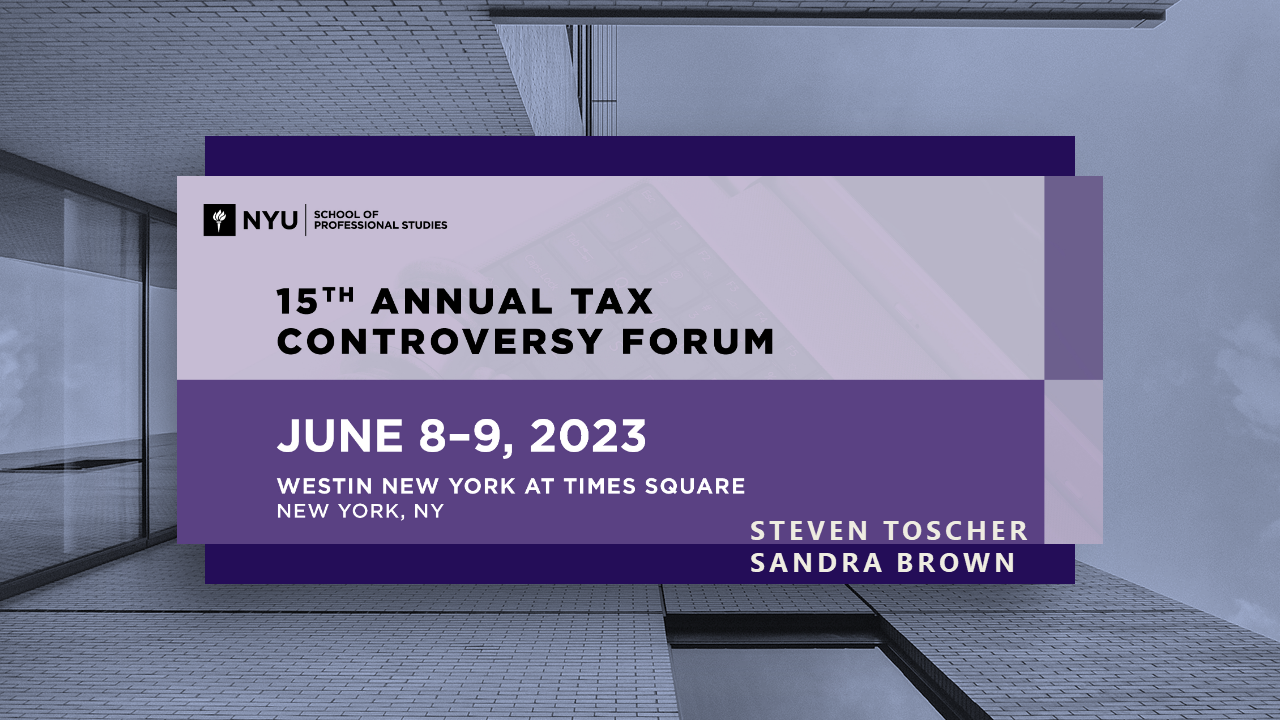

Read MoreNYU 15th Annual Tax Controversy Forum and Agostino & Associates BBQ and Seminar

We are pleased to invite you to register now for the 15th Annual NYU Tax Controversy Forum to be held June 8 and 9 Westin New York, Times Square You do not want to miss this program. Two of our principals will be speaking on the following topics: Sandra Brown Employee Retention Credit Audits and […] Read More…

Read MoreROBERT HORWITZ and JONATHAN KALINSKI to Speak at Upcoming CalCPA Webinar

We are pleased to announce that Robert Horwitz and Jonathan Kalinski will be speaking at the upcoming CalCPA webinar “Handling Partnership Examinations – WYNTK About New Partnership Procedural Rules,” Tuesday, May 23, 2023, 9:00 a.m. – 10:00 p.m. (PST). This webinar will cover practical considerations for partners and advisers to partnerships operating under the new partnership […] Read More…

Read More“IRS Announces Plans to Issue New Crypto Tax Guidance” – What it Means for the Industry By PHILIPP BEHRENDT

At the end of last year, the IRS has established a digital asset project office to address crypto-related issues, and it has already begun business. The move reflects the IRS’s growing recognition of the importance of cryptocurrencies and the need for clear guidelines for their taxation.[1] Julie Foerster, who leads the office, recently spoke at […] Read More…

Read MoreEDWARD M. ROBBINS, JR. and JONATHAN KALINSKI to Speak at Upcoming BHBA Webinar

We are pleased to announce that Edward M. Robbins, Jr. and Jonathan Kalnski will be speaking at the upcoming Beverly Hills Bar Association webinar “IRS International Penalties After Farhy,” Thursday, May 18, 2023, 12:00 p.m. – 1:30 p.m. (PST). On April 3, 2023, the United States Tax Court, in Farhy v. Commissioner held that the IRS has […] Read More…

Read MoreCalifornia Lawyers Association – 2023 Washington D.C. Delegation and U.S. Supreme Court Group Swearing-In Event – May 15-18, 2023

We are very pleased to announce that Sandra R. Brown, Robert Horwitz, Michel Stein, Edward M. Robbins, Jr., Philipp Behrendt, Gary Markarian, and Michael Greenwade will be part of the Taxation Section of the California Lawyers Association’s “DC Delegation” on May 16-17, 2023, in Washington D.C. For over 30 years, the Taxation Section has annually […] Read More…

Read MoreSave the Date – UCLA 39th Annual Tax Controversy Institute – October 26, 2023

Dear Colleague- We cordially invite you to save the date for this years UCLA Extension Tax Controversy Institute which will be live this year and held on October 26, 2023 at the Beverly Hills Hotel in Beverly Hills, California. The Institute is entering its 39th year and is recognized as one of the top tax controversy […] Read More…

Read MoreMICHEL STEIN, EVAN DAVIS and PHILIPP BEHRENDT to Speak at Upcoming CPA Academy Webinar

We are pleased to announce that Michel Stein, Evan Davis and Philipp Behrendt will be speaking at the upcoming CPA Academy webinar “New Developments in Cryptocurrency: Reporting and Enforcement,” Thursday, May 11, 2023, 8:00 a.m. – 9:00 a.m. (PST). This program will provide tax advisers and compliance professionals with a practical look at IRS guidance for calculating […] Read More…

Read MoreSTEVEN TOSCHER, MICHEL STEIN and CORY STIGILE to Speak at Upcoming Strafford Webinar

We are pleased to announce that Steven Toscher, Michel Stein and Cory Stigile will be speaking at the upcoming Strafford webinar “IRS High-Wealth Examinations: IRS Wealth Squad, Targeted Issues, Preparation, IDRs, Appeals, and Litigation,” Thursday, May 4, 2023, 10:00 a.m. – 11:50 a.m. (PST). The IRS Large Business and International Division is auditing high net worth individuals and their […] Read More…

Read More