TAXLITIGATOR Blog

Hochman Salkin Toscher Perez P.C. Attorneys Recognized by 2023 Super Lawyers in Taxation

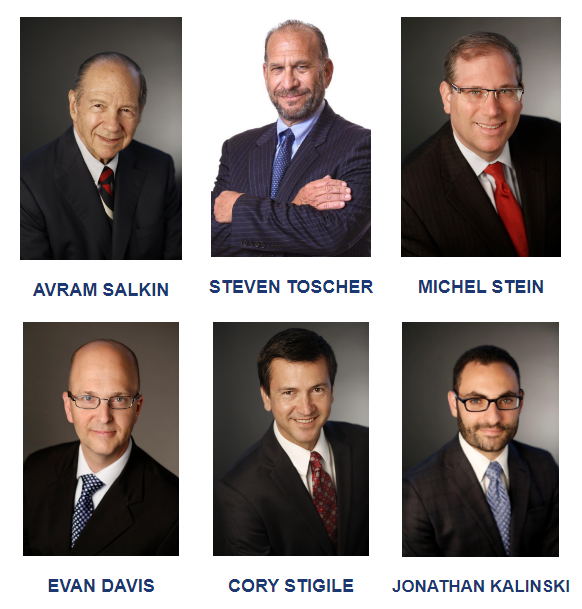

We are pleased to announce that 6 of our principals have been selected to the 2023 Southern California Super Lawyers List in the field of Taxation. Attorneys selected as Super Lawyers are among the top five percent of Southern California’s licensed attorneys. Southern California Super Lawyers Magazine recognizes outstanding attorneys in more than 70 areas of practice […] Read More…

Read MoreDon’t Forget the Requirement to File an Administrative Claim for the Refund of Taxes by PHILIPP BEHRENDT

On January 11, 2023, the United States District Court for the Western District of New York ruled on the case of United States v. Chen-Baker, Case. No. 1:22-cv-256. This case provides an important reminder of the importance for individuals or organizations in filing administrative claims against the government before suing the government. This case involves […] Read More…

Read MoreMICHEL STEIN, SANDRA BROWN and EVAN DAVIS to Speak at Upcoming ABA Midyear 2023 Tax Meeting

Please join us February 9-11, 2023 for the ABA Midyear 2023 Meeting at the Hilton San Diego Bayfront. Our firm is proud to continue our participation. Meet with fellow tax practitioners and address the cutting-edge tax issues affecting all tax professionals. This three-day event includes discussions, networking opportunities led by the best tax professionals in the nation, covering various topics. […] Read More…

Read MoreSTEVEN TOSCHER, SANDRA BROWN and JONATHAN KALINSKI to Speak at Upcoming Strafford Webinar

We are pleased to announce that Steven Toscher , Sandra Brown and Jonathan Kalinski will be speaking at the upcoming Strafford webinar “Taxation of Cannabis: Overcoming Tax Challenges in Cannabis Business Operations, Key Planning Techniques,” Tuesday, January 17, 2023, 10:00 a.m. – 11:30 a.m. (PST). The sale and distribution of cannabis for recreational or medical use has become a […] Read More…

Read MoreCalifornia Board of Legal Specialization of the State Bar of California Recognizes Our Lawyers

We congratulate the lawyers at our firm who have been honored by the California Board of Legal Specialization of the State Bar of California with acknowledgment of at least 20 years of continued professional participation and advancement as Certified Specialists in Taxation Law HSTP is proud to encourage its lawyers to seek and maintain professional […] Read More…

Read MoreUSC Gould School of Law 70th Tax Institute – January 23-25, 2023

Please join us January 23-25, 2023 for the USC Gould School of Law 2023 Tax Institute at the Millennium Biltmore Hotel, Los Angeles. This is the Institute’s 70th year and the firm is proud to continue our participation. Meet with fellow tax practitioners and address the cutting-edge tax issues affecting all tax professionals. This three-day institute includes discussions, networking opportunities […] Read More…

Read MoreIRS Issues Proposed Regulation on Conservation Easements as Listed Transactions, but that Doesn’t Mean It Is Acquiescing to Court Decisions by ROBERT S. HORWITZ

In Green Valley Investors, LLC v. Commissioner, 159 T.C. No. 5 (Nov. 9, 2022), the Tax Court invalidated Notice 2017-10, which designated syndicated conservation easements as listed transactions, because it was a legislative rule that was issued without complying with the notice and comment provisions of the Administrative Procedures Act (“APA”). We recently blogged on […] Read More…

Read MoreSTEVEN TOSCHER Elected to Tierra Del Sol Foundation’s Board of Directors

Click Here to Read More

Read MoreHappy Holidays from Hochman Salkin Toscher Perez P.C.

Read More

Read More

CORY STIGILE and PHILIPP BEHRENDT to Speak at Upcoming Beverly Hills Bar Association Webinar

We are pleased to announce that Cory Stigile and Philipp Behrendt, will be speaking at the upcoming BHBA webinar “The Ins and Outs of Tax Audits,” Tuesday, January 10, 2023, 12:30 p.m. – 1:30 p.m. (PST). This program will go over the fundamentals of tax audits in order to provide business owners, entrepreneurs, and practitioners with the tools and language […] Read More…

Read MoreABA National Institute on Criminal Tax Fraud & Tax Controversy Conference – Tax Court’s Pro Bono Calendar Call

Read More

Read More

No Equitable Tolling for Deficiency Cases: The Tax Court Holds that the Period of Limitations for Filing a Petition to Redetermine a Deficiency Is Jurisdictional by ROBERT S. HORWITZ

In Boechler v Commissioner, 596 U.S. ___, 142 S.Ct. 1493 (2022), the Supreme Court held that the 30-day period for petitioning the Tax Court to review a collection due process determination was not jurisdictional and, therefore, could be equitably tolled. Following the Boechler decision, several bloggers, including me, questioned whether the time period of filing […] Read More…

Read More